What Older Americans Want From Workplace Investing

Ideas for Improving Advice & Income Products

Order Report - What Older Americans Want From Workplace Investing: Ideas for Improving Advice & Income Products

Overview

This report is from the Hearts & Wallets research collection focusing on saving, investing and advice and leverages analytics and datasets from two proprietary databases - Investor QuantitativeTM and Explore QualitativeTM. It will be of particular interest to those who work on advice, retirement, retirement income, rollover and client experience for older consumers.

Older Americans are looking for advice on everything including work, retirement planning, investing, housing and tax optimization. But most are reliant on retail sources of advice vs. what is offered through the workplace. Find out why. Learn consumers biggest complaints, suggested fixes, and possible solutions for bridging the gap between wants and current workplace offerings.

The new 76 page report features 38 exhibits. See table of contents and sample pages below.

Key Findings

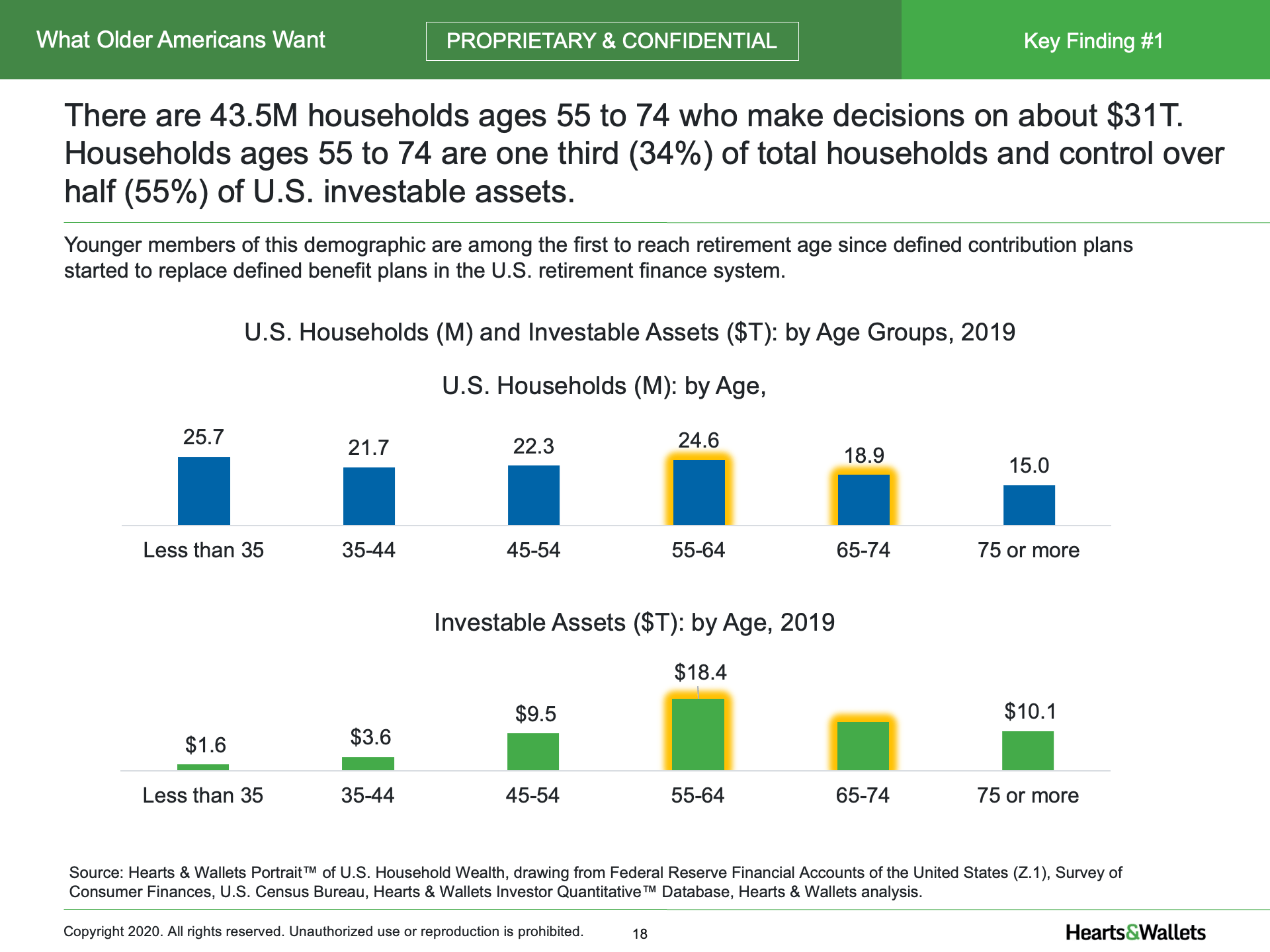

- The 43.5M households age 55-74 control $31T, or 55%, of all investable assets in the U.S. As navigating life beyond age 55 becomes more challenging without the pension safety net, older Americans are looking for advice on topics including work, retirement planning, investing, housing and tax optimization.

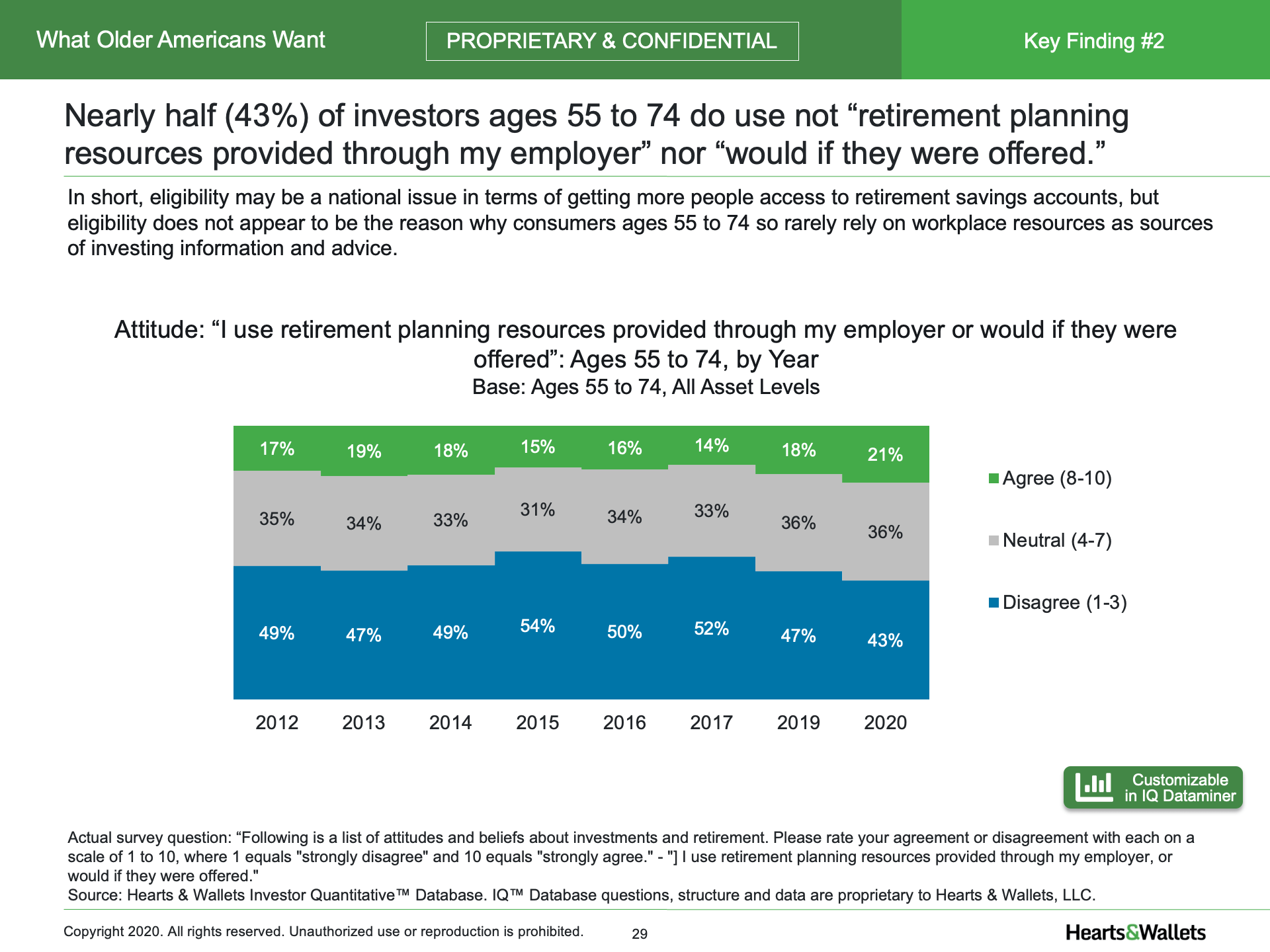

- Most people age 55+ are much less engaged with workplace resources than other sources of investing information and advice. Eligibility is not the main barrier: nearly half of investors ages 55 to 74 do not use “retirement planning resources provided through my employer” nor “would if they were offered.”

- Older affluent consumers reported 6 glaring complaints and disconnects as the reasons current workplace resources aren’t working for them.

- Older affluent consumers offered 6 suggestions for employers and financial services companies who are committed to serving them through workplace.

- Analysis of customer experience shows higher intent to recommend retail than workplace relationships. Lower results for workplace, plus facts that confirm consumer-reported gaps in advice on housing, work outlook and tax optimization, indicate that leaving money in plan for income and getting broader advice in retail may be the best approach.

Convenient Options to Suit Your Needs and Budget

Choose access licenses for your team or organization in ways that support how you collaborate. AVAILABLE FOR LICENSE TO NON TRENDS SUBSCRIBERS OCT. 15, 2020

Sample Pages

Table of Contents

Executive Summary

Methodology

Key Findings and Implications, Favorite Statistics, Related Research

Key Finding #1: As navigating life beyond age 55 becomes more challenging without the pension safety net, older Americans are looking for advice on housing, work outlook and tax optimization.

1.1 U.S. Households (M) and Investable Assets ($T): by Age Groups, 2019

1.2 U.S. Households (M) and Investable Assets ($T): Ages 55 to 74 by Investable Asset Groups, 2019

1.3 Crosstab: Actual Replacement Rate by Concern “Making Ends Meet”: Post-Retirees, Ages 55 to 74, 2020

1.4 Crosstab: Actual Replacement Rate by Feelings about Financial Security: Post-Retirees, Ages 55 to 74, 2020

1.5 Actual Replacement Rate and Sources of Income: Post Retirees, Ages 55 to 74, by Investable Asset Groups, 2020

1.6 Percent of Income in Retirement from Pensions by Age of Stopping Full-Time Work: 2020

1.7 Anticipated Replacement Rate and Sources of Income: Late Career, Pre-Retiree, Fully Employed Seniors, Ages 55 to 74, by Investable Asset Groups, 2020

1.8 Selected Account Types Ownership Rates: Ages 55 to 64 and Ages 65 to 74, by Investable Asset Groups: 2019

1.9 Selected Real Estate Statistics: Ages 55 to 74, by Investable Asset Groups, 2015-2020

1.10 Explore Qualitative Exercise: Expectations for Financial Services from Workplace vs. Retail – Want vs. Get Ratio

Key Finding #2: Most people age 55+ are much less engaged with workplace resources than other sources of investing information and advice.

2.1 Sources of Investing Information and Advice – Reliance on “Employer-sponsored programs, including 401(k) or 403(b) provider and its representatives” (“Workplace”): by Breadwinner Age Groups, 2020

2.2 Attitude: “I use retirement planning resources provided through my employer or would if they were offered”: Ages 55 to 74, by Year

2.3 Sources of Investing Information and Advice – Reliance on “Employer-sponsored programs, including 401(k) or 403(b) provider and its representatives”: Among Eligible and Participating in Employer Plan, Ages 55 to 74, by Year

2.4 Sources of Investing Information and Advice – Reliance on “Employer-sponsored programs, including 401(k) or 403(b) provider and its representatives”: Segmented by Investable Asset Groups and Participation in Employer Plan, Ages 55 to 74, 2020

2.5 Compare Selected Sources of Investing Information and Advice – Reliance: Ages 55 to 74, All Asset Levels, 2020

2.6 Compare Selected Sources of Investing Information and Advice – Reliance: Ages 55 to 74, $500K-<$3M Investable Assets, 2020

2.7 Compare Selected Sources of Investing Information and Advice – Reliance: Ages 55 to 74, $100K-<500K Investable Assets, 2020

2.8 Compare Selected Sources of Investing Information and Advice – Reliance: Ages 55 to 74, <$100K Investable Assets: 2020

2.9 Crosstab - Agreement with Attitude “I understand where my income during retirement will come from” by Reliance on Workplace and Paid Investment Professional (Net): Ages 55 to 74, 2019

Key Finding #3: Older affluent consumers reported 6 glaring complaints and disconnects as the reasons current workplace resources aren’t working for them.

3.1 Explore Qualitative Exercise: Expectations for Financial Services from Workplace vs. Retail – Summary of Older Affluent Consumer Issues with Workplace Saving & Investing Advice

3.2 The fact that workplace saving and investing programs must be generic for all employees irks older affluent consumers…

3.3 The fact that workplace programs are generic gives them the feeling they can’t get what they want from workplace saving and investing solutions.

3.4 Perceptions that reps are inexperienced can give a bad impression. Older affluent consumers have decades of experience managing their finances, so even a rep with 5 to 10 years of experience can seem inexperienced to them.

3.5 Little or no proactive outreach gives older affluent consumers the impression that workplace saving and investing providers don’t care about them or their business.

3.6 Many participants feel saving and investing is not their employer’s area of expertise and they shouldn’t be trying to do it.

3.7 Some participants pointed out that, once you’ve retired, you’re no longer connected to your employer.

3.8 Some participants said, “I don’t want my employer involved in my finances.” what

Key Finding #4: Older affluent consumers suggest 6 fixes for employers and financial services companies who are committed to serving them through workplace.

4.1 Explore Qualitative Exercise: Expectations for Financial Services from Workplace vs. Retail – Summary of Consumer Suggested Ways to Improve Workplace Retirement Advice.

4.2 Older affluent participants know pensions are valuable. Those who have pension income feel “lucky.”

4.3 Participants said that good advice must be comprehensive, whether it’s provided by employers or by resources they find on their own.

4.4 Many of the participants were self-employed to some degree. Feelings of desire to understand human capital are energetic and urgent.

4.5 Older Americans who understand the dynamics of workplace retirement plans see employer legal liability that limits quality of advice and incentives as a problem.

4.6 Lack of clarity around provider incentives is widely acknowledged as a problem. This creates skepticism and makes consumers feel “leery.” and

4.7 Participants express frustration that pressures on workplace pricing limit choice. They are interested in paying more to get more, if fees were clearer.

Key Finding #5: Analysis of customer experience shows higher intent to recommend retail than workplace relationships. This, plus facts that confirm consumer-reported gaps in advice on housing, work outlook and tax optimization, indicates that leaving money in plan and getting broader advice in retail may be the best approach.

5.1 Crosstab - Percent of Actual Retirement Income from Pensions and Feelings of Financial Security: Post-Retirees, Ages 55 to 74, 2020

5.2 Attitude "I am comfortable leaving money in a retirement plan sponsored by a company where I no longer work”: Ages 55 to 74, by Year

5.3 Attitude "I am comfortable leaving money in a retirement plan sponsored by a company where I no longer work”: Ages 55 to 74, by Investable Asset Groups, by Year

5.4 Spending by Category: Ages 55 to 74, by Investable Asset Groups, 2020

5.5 Crosstab: Percent of Spending on Housing & Utilities and Feelings of Financial Security: Ages 55 to 74, 2020

5.6 Breadwinner Retirement Age – Actual and Anticipated: 2020

5.7 Work-Retirement Spectrum: Ages 55 to 64 and 65 to 74, by Investable Asset Groups, 2020

5.8 Retirement Income Plan Component – “Recommendations for minimizing your tax obligations during retirement”: Ages 55 to 74, by Investable Asset Groups, 2016

5.9 Intent to Recommend Primary & Secondary Stores: Ages 55 to 74, All Asset Levels, by Year

5.10 Selected Statistics on Workplace and Retail: Ages 55-74, $500K-<$3M, by Year

5.11 Selected Account Type Ownership Rates - Rollover IRAs, Current and Former Employer-Sponsored Retirement Plans: Ages 55 to 64 and Ages 65 to 74, by Investable Asset Groups, 2019

5.12 Selected Statistics on Workplace and Retail: Ages 55 to 74, $100K-<$500K Investable Assets, by Year

5.13 Selected Statistics on Workplace and Retail: Ages 55 to 74, <$100K Investable Assets, by Year

Appendix:

Data Dictionary

Glossary, Sample Sizes

Use Contact Us form below to request more information. We look forward to hearing from you!

*Clients must demonstrate appropriate standards of use and library controls to be eligible for Enterprise+. In addition to the PDF for storage in internal reference library, Enterprise+ users may also access the Hearts & Wallets Client Portal and slide download features.