Financial Fluency

What Consumer Understanding of the Language of Finance Means for Advice, Retirement and Asset Management

Order Report - Financial Fluency: What Consumer Understanding of the Language of Finance Means for Advice, Retirement and Asset Management

Overview

The language of investing is complex. Despite all the efforts within the industry to simplify it and make investing concepts and more easily understood, we are failing. Investors are still confused - 81% consumers lack financial fluency.

More specifically, fluency is much higher for consumers with higher assets and higher education levels; men have better understanding than women across all asset levels and Consumers who feel “experienced” at investing are decidedly more fluent. Retirement plan participants have the most challenges and lack the fluency to select investments.

The new 62 page report features 49 exhibits. See table of contents and sample pages below.

Key Findings

- The language of investing is poorly understood. One way to improve fluency is to work with advisors

- Most workplace retirement plan participants face a challenge because most lack sufficient fluency to select investments required or allowed by most plans

- Lack of language clarity causes financial damage. Consumers confused by competing definitions for “passive investing” save less and use fewer products

- The complexity of taxes presents an opportunity for higher value-add advice

- When the technical language to explain complex choices is too difficult to understand, new concepts are needed

Convenient Options to Suit Your Needs and Budget

Choose access licenses for your team or organization in ways that support how you collaborate. AVAILABLE FOR LICENSE TO NON TRENDS SUBSCRIBERS OCT. 15, 2020

- Online with slide download, PPT & PDF (unlimited log-ins) - $18,000

- Online with slide download (1-50 logs-ins) - $12,000

- Online only (1-20 log-ins) - $9,000

Sample Pages

Table of Contents

Executive Summary

Methodology

Key Findings and Implications

Favorite Statistics

Related Research

Key Findings

1: The language of investing is poorly understood. One way to improve fluency is to work with advisors

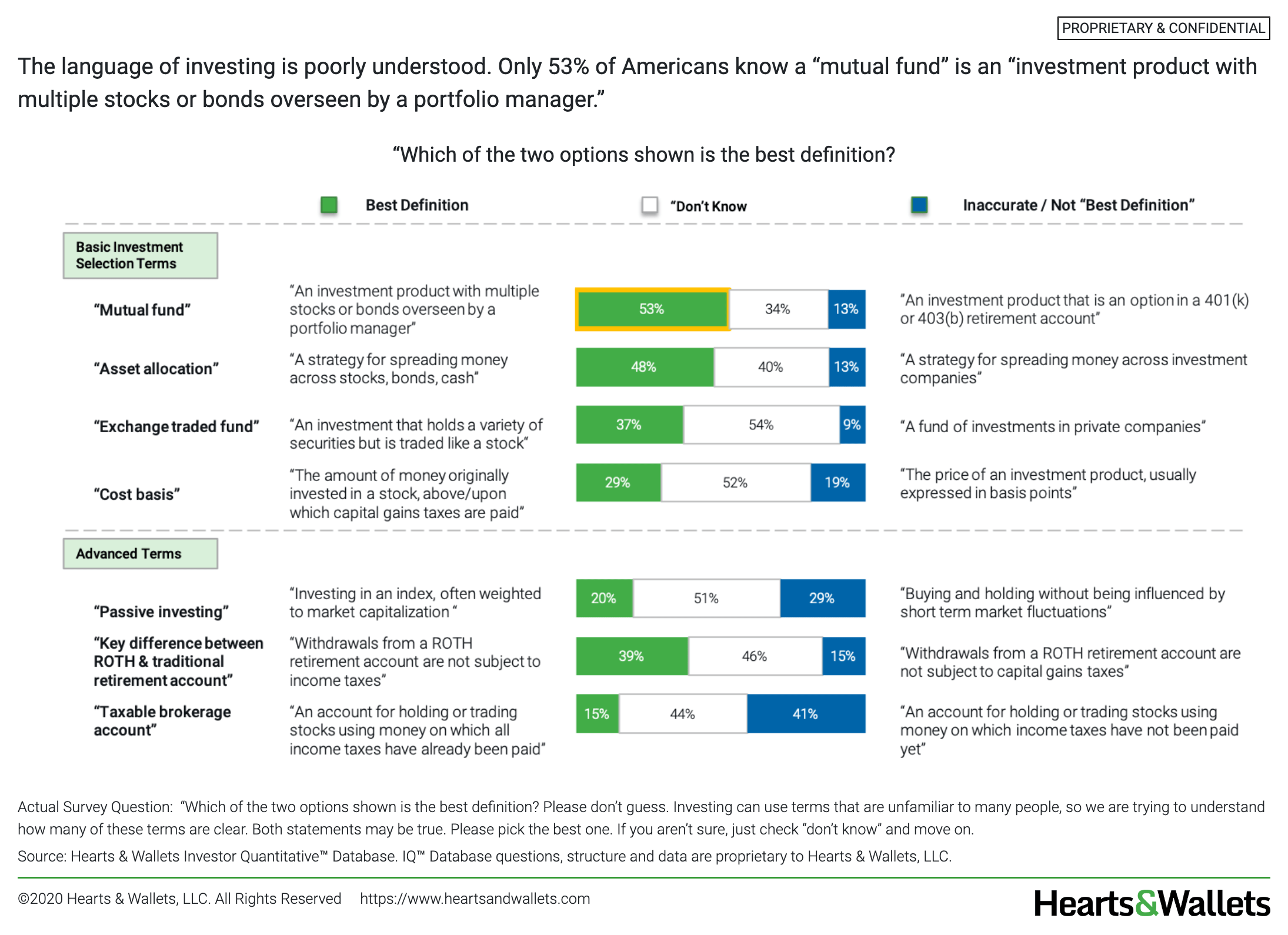

1.1: The language of investing is poorly understood. Only 53% of Americans know a “mutual fund” is an “investment product with multiple stocks or bonds overseen by a portfolio manager.”

1.2: Most consumers (81%) lack fluency with investing terms

1.3: Age improves understanding of investing language, but only ever so slightly

1.4: Pre-Retirees are the most fluent, but only slightly more than other lifestages

1.5: Fluency is higher among married respondents

1.6: Consumers with more education are more fluent than consumers with less education

1.7: Three of 10 consumers (30%) who identify as self-directed investors did not know the best definition for even one term

1.8: Consumers with higher assets are more fluent than lower-asset consumers

1.9: Gender affects fluency. Twice as many men as women got 5 or more correct. One in 3 female respondents got none correct

1.10: Men have better understanding than women across all asset levels

1.11: Women are more likely than men to respond “don’t know” for two or more terms

1.12: Consumers who feel “experienced” at investing are decidedly more fluent

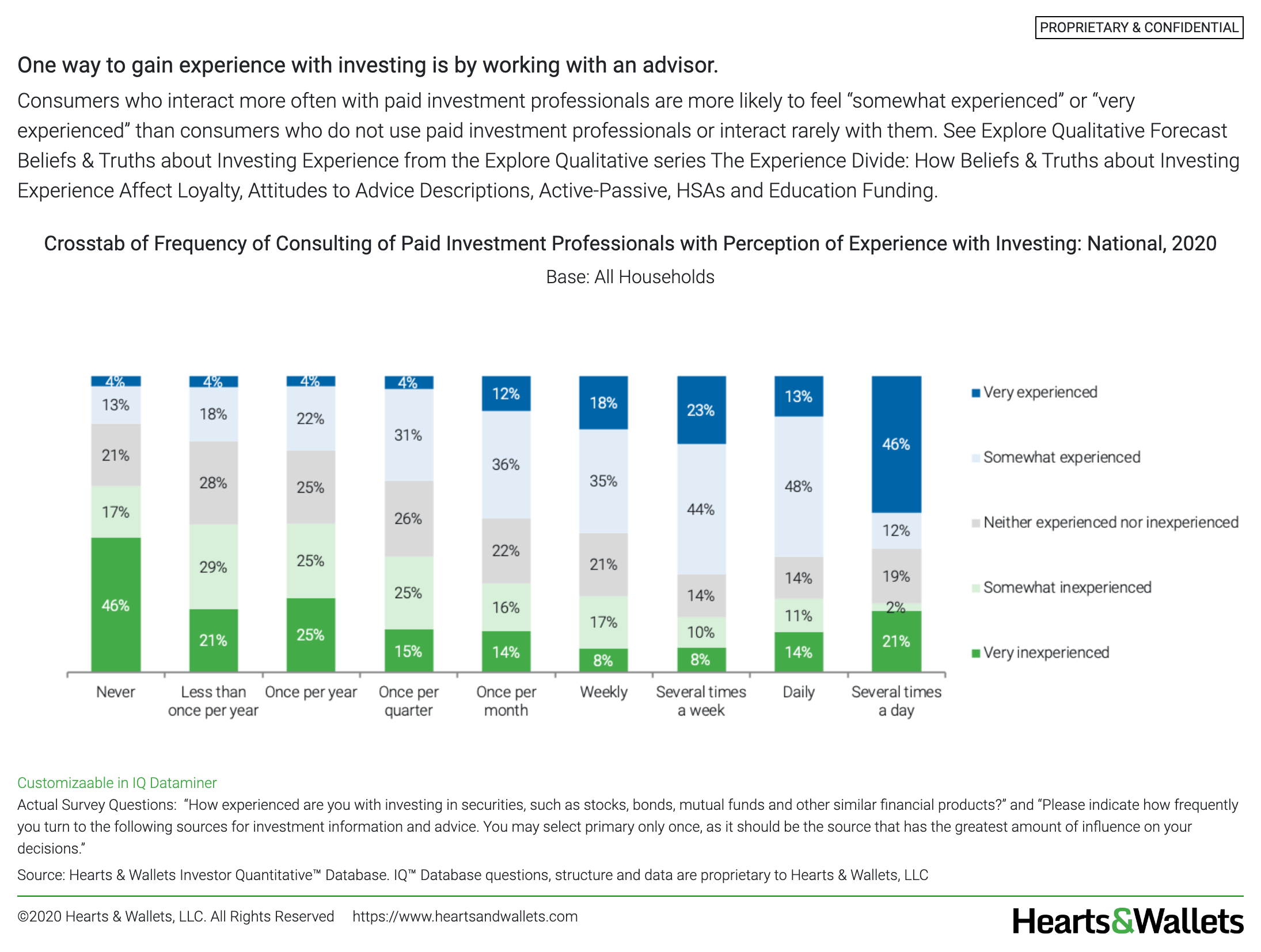

1.13: One way to gain experience with investing is by working with an advisor

1.14: Consumers who use advisors regularly are more fluent than consumers who do not

1.15: Being in regular communication with a paid investment professional improves fluency among lower-asset groups

2: Most workplace retirement plan participants face a challenge because most lack sufficient fluency to select investments required or allowed by most plans

2.1: The four basic investment selection terms are important for retirement plan participants because participants are responsible for picking their own funds and these terms are fundamental to their ability to select investments

2.2: One in 3 (29%) potential participants in workplace retirement plans did not know any of the definitions for the 4 basic investment selection terms

2.3: Language barriers may be deterring eligible participants from plan participation. More participants who are eligible but not participating do not know the best definition for any of the terms vs. participants (38% vs. 29%)

2.4: The language barrier is most acute among plan participants with less than $100K in total assets. Many participants with $100K-<$500K also face language barriers

2.5: Millennial plan participants need the most help in understanding basic concepts, but results are low across all generations

2.6: Understanding of basic investment selection terms is lower among female participants than male participants. Less than 1 in 3 women (29%) correctly understood 3+ terms vs. 43% of males

2.7: In a distressing twist, participants with no pensions are less likely to understand basic definitions than participants with at least some pension income

2.8: Unfortunately, workplace programs, as currently structured, do not improve fluency with basic investment selection terms

2.9: Building fluency with basic investment selection terms will provide benefits to financial behaviors that extend beyond the retirement plan

2.10: Better fluency with basic investment selection terms is associated with better financial wellness, including better funded emergency funds

2.11: Within the income range $48K-<$96K, participants who are more fluent in basic investment selection terms have more months of funded emergency funds

3: Lack of language clarity causes financial damage. Consumers confused by competing definitions for “passive investing” save less and use fewer products

3.1: Turning to the term “passive investing,” a nuanced concept that guides investing strategy, half of all consumers do not know the definition. Of consumers who chose a definition, more picked ”buy and hold” than “invest in an index”

3.2: “Buy and hold” resonated more than “invest in an index” across all generations as the best definition of “passive investing.” Then again, half of consumers did not pick between the two definitions and instead selected “don’t know"

3.3: Consumers who consider themselves “experienced” investors are more likely to pick the technical “invest in an index” definition rather than the intuitive “buy and hold” definition.

3.4: Consumers who “don’t know” the definition of “passive investing” are more likely than consumers who picked a definition to have high cash allocation and lack exposure to the stock market

3.5: Consumers who “don’t know” what “passive investing” means are unlikely to own mutual funds, historically one of the easiest products retail investors can use to gain access to capital markets

3.6: Consumers who “don’t know” what ”passive investing” means save less than consumers who pick either “invest in an index” or “buy and hold"

3.7: Consumers who “don’t know” what “passive investing” means are less likely to have online brokerage accounts than consumers who picked “invest in an index” or “buy and hold”

3.8: Consumers who “don’t know” what “passive investing” means are less likely to “have a retirement savings plan and contribute to it regularly"

3.9: Consumers who “don’t know” what “passive investing” means are less likely to allocate any savings to IRAs

3.10: Consumers who “don’t know” what “passive investing” means are more likely to not “feel on track to accumulating the savings I’ll need to retire"

3.11: Most stores have a significant number of customers who “don’t know” and are therefore at risk of language confusion holding them back from being engaged with saving and capital markets, both necessary to achieve financial success

3.12: The intuitive definition is displacing the technical one to such a degree that even 37% of consumers who own exchange-traded funds (ETFs) selected “buy and hold"

3.13: Most stores can expect that most of their customers embrace the intuitive “buy and hold” definition of “passive investing"

4: The complexity of taxes presents an opportunity for higher value-add advice

4.1: The complexity of taxes presents an opportunity for higher value-add advice

4.2: Inside Advice® Benchmarking finds that almost no advice and guidance experiences currently offer tax optimization

4.3: A key reason for participating in employer-sponsored retirement plans is “benefit from tax deferral"

4.4: “Benefit from tax deferral” is more important to workplace plan participants in upper income levels

4.5: Consumers are likely to prioritize immediate tax considerations over longer-term tax optimization when they allocate saving across account types

4.6: As they near retirement, older people become more aware of the importance of taxes and want to optimize taxes

4.7: Tax optimization advice is a big unmet need once consumers become aware of it

5: When the technical language to explain complex choices is too difficult to understand, new concepts are needed

5.1: The car industry provides an interesting example of how developing new, easier-to-understand concepts, such as categories, can relieve the difficulty of explaining complex language necessary for consumers to understand technical features

5.2: Complex concepts require complex language. In investing as in cars, consumers will likely be more empowered by new shared concepts for which language can be more intuitive vs. attempting to provide fluency in existing technical language

5.3: The simplicity of the concept and the language is why the majority of consumers like Inside Advice® Grid, and 1 in 6 likes it very much. The remainder are largely neutral and open, ready to hear more

Data Dictionary

Appendix

Glossary

Use Contact Us form below to request more information. We look forward to hearing from you!

*Clients must demonstrate appropriate standards of use and library controls to be eligible for Enterprise+. In addition to the PDF for storage in internal reference library, Enterprise+ users may also access the Hearts & Wallets Client Portal and slide download features.